Meals & Entertainment ExpensesUnder the One Big Beautiful Bill Act

2/18/2026 - By David Uslan, CPA

{kind=link}

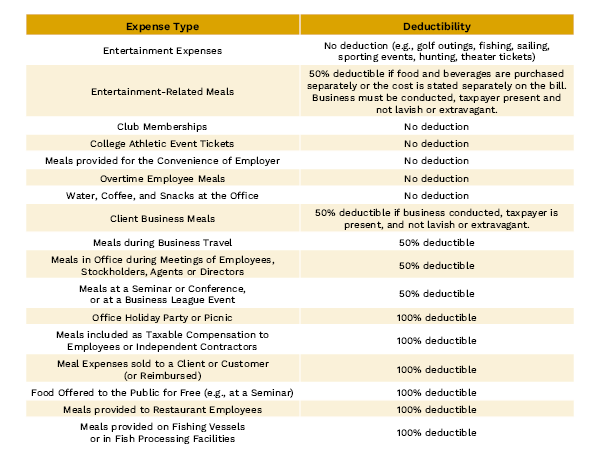

The One Big Beautiful Bill Act (OBBBA) made changes to a company’s ability to deduct certain meal and entertainment expenses, especially for meals provided to the employees for the convience of the employer. A chart is provided below, to summarize proper treatment for many types of meal and entertainment expenditures, under the OBBBA.

Our recommendation is to be more diligent in the classification of meal and entertainment expenses of 2026 and beyond. Since some of these expenses will no longer be deductible, these expenses should be segregated into different accounts for tracking (e.g., 0% meals, 50% meals, 100% meals, and non-deductible entertainment).

The meal and entertainment changes under the One Big Beautiful Bill Act (OBBBA) are just one piece of a broader tax landscape shift. For a deeper understanding of how OBBBA may impact your business beyond meals and entertainment, read our overview blog, “Tax Law Impacts: One Big Beautiful Bill Act”.

If you have questions about properly classifying expenses, updating your chart of accounts, or preparing for 2026 and beyond, contact our expert tax team at Saltmarsh to discuss your specific situation.

About the Author | David Uslan, CPA

David is a partner and the tax technical leader with experience across tax, accounting, and advisory services. He began his career in public accounting over 30 years ago, focusing on serving high-net-worth individuals and growth-oriented companies. His primary areas of experience include providing tax and advisory services to clients in the software, real estate, private equity, professional services, technology, and creative services industries.

Related Posts

- Family Office Tax Planning

- Funding Liquidity Without Triggering Capital Gains

- Could You Be Owed a Refund for IRS Penalties or Interest During Covid?

- IRS Notice CP53E: What Is It & What to Do If You Receive One

- Introducing Our New Podcast: Integrated Wealth Perspectives

- Outsourced Accounting for Nonprofits

- Manufacturing Cash Flow Forecasting Services for Volatile Markets

- Church Accounting Services for Donor Tracking & Financial Transparency

- Real Estate Accounting Services for Cash Flow Visibility and Portfolio Performance

- Maximizing Your Home Office Deduction

- What CEOs and CFOs Need to Know About Outsourced Accounting Costs

- How Outsourced Accounting Helps Growing Businesses Scale with Confidence

- Are You 5500 Compliant? Key Considerations for Health & Welfare Plans

- Avoid Costly Bookkeeping Mistakes in Your Construction Projects

- What the Best Accounting Outsourcing Companies Provide that Bookkeepers Don't

- How an Outsourced Accounting Department Transforms Month-End Close

- Meals & Entertainment Expenses

- How Accounts Payable Outsourcing Improves Accuracy, Speed, and Internal Controls

- The Hidden Benefits of Accounts Receivable Outsourcing for Businesses

- IRS Releases FAQ on Paper Check Phase-Out

- Construction Accounting Methods Explained: Cash, Accrual, and Percentage-of-Completion

- Saltmarsh Leader Suzanne Bach Joins ABC Florida Gulf Coast Board

- The Final Chapter of the Estate Plan

- What to Know Before Year-End

- The End of Paper Refund Checks: Are You Ready for the IRS Digital Shift?

- View All Articles