Funding Liquidity Without Triggering Capital GainsHow a Pledged Asset Line & the Step-Up in Basis can Work Together at Death

6/8/2026 - By Michael Hall

{kind=link}

Clients with concentrated, highly appreciated positions often need cash without wanting to sell. Selling triggers capital gains tax today and removes shares that would otherwise receive a step-up in cost basis at death. A pledged asset line lets a client borrow against the portfolio instead. Pledging securities as collateral is not a sale, so it creates no taxable event, and the position stays invested and eligible for the basis reset.

A Hypothetical Comparison

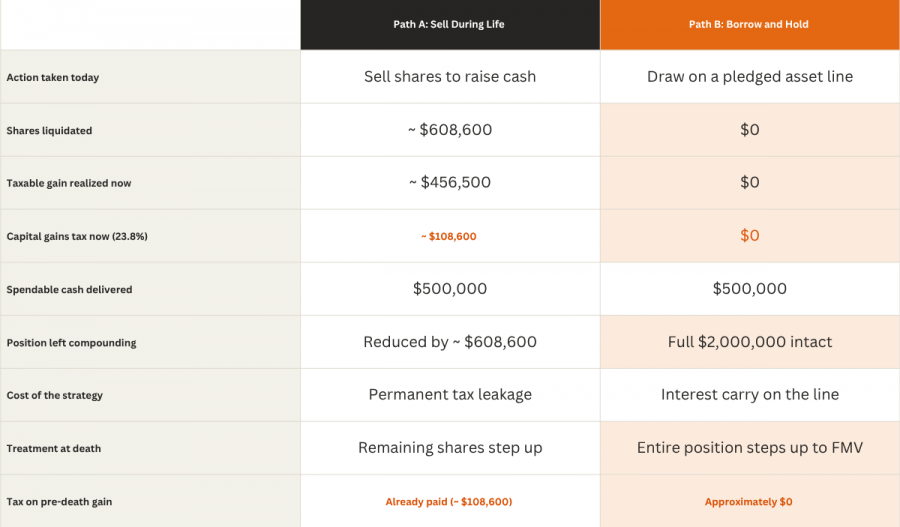

A client holds a $2,000,000 position with a $500,000 cost basis (a $1,500,000 unrealized gain) and needs $500,000 of spendable cash. Florida has no state income tax, so the combined federal long-term capital gains and net investment income tax rate is 23.8%.

Why the Difference

At death, securities included in the estate are revalued to fair market value under Internal Revenue Code Section 1014. The embedded gain on the pre-death appreciation is erased. Heirs can then sell stepped-up shares to retire the line with little or no capital gains tax. The loan itself is never a taxable event; repaying it is simply the satisfaction of a debt. In Path B, roughly $108,600 of capital gains tax on the liquidity slice is deferred during life and then permanently avoided at death, while the full $2,000,000 keeps compounding.

For clients with a taxable estate, the outstanding loan balance is also a deductible claim against the estate under Section 2053, reducing the gross estate dollar for dollar.

Key Risks and Considerations

The benefit depends on holding the position until death. A market decline that breaches the line's maintenance requirement can force a sale of collateral at an inopportune time, realizing gains during life. Interest accrues for as long as the line is drawn and reduces the net advantage. Account titling matters: for assets held jointly with a spouse in Florida, generally only the decedent's half steps up at the first death. The step-up eliminates income tax on the appreciation, but it does not erase the debt, so net wealth to heirs is still reduced by the loan balance.

Interested in how today’s market changes could impact your long-term investment strategy? The Saltmarsh Financial Advisors team can help you evaluate opportunities through a disciplined, fundamentals-based approach designed around your goals. Connect with our advisors to discuss your portfolio, risk tolerance, and long-term financial plan.

About the Author | Michael C. Hall, CFP®

Michael is a director for Saltmarsh Financial Advisors, LLC, an affiliate of Saltmarsh. With over 22 years of expertise in asset management and financial planning, he specializes in delivering comprehensive wealth management solutions that integrate asset management with tax planning and risk management. He works closely to ensure that each client’s financial goals are met with a comprehensive plan and strategies tailored to their unique risk tolerance, growth objectives, and overall financial well-being.

This material is for educational and illustrative purposes only and does not constitute tax, legal, or investment advice. The figures are hypothetical and assume a single individual owner of a taxable account who holds the position until death, a 25% basis ratio, and a combined 23.8% federal long-term capital gains and net investment income tax rate with no state income tax. Actual outcomes will vary with basis, holding period, tax rates, interest costs, market performance, and account titling. Borrowing against securities involves risk, including a maintenance call that may force the sale of collateral and realize gains during life. Consult your Saltmarsh advisor and qualified tax and legal counsel before acting. Saltmarsh Financial Advisors is a registered investment advisor. Tax law is current as of 2026.

Related Posts

- Long-Term Care Planning: Protecting Your Retirement, Your Assets & Your Family

- A Quarter of Reversal: Markets & the Economy in the Second Quarter of 2026

- Saltmarsh Financial Advisors Earns World-Class Client Satisfaction

- When Wealth Means More: The Keys to Establishing a Lasting Legacy

- Funding Liquidity Without Triggering Capital Gains

- Saltmarsh Financial Advisors Hosts Client Appreciation Night at the Ballpark in Pensacola

- Beyond the Hype: What the Coming Mega-IPOs Mean for Your Portfolio

- Introducing Our New Podcast: Integrated Wealth Perspectives

- Financial Scams are Evolving

- Saltmarsh Financial Advisors Earns World-Class Client Satisfaction

- The Final Chapter of the Estate Plan

- How to Prepare for a Spouse's Passing: Practical Steps for Peace of Mind

- What to Do After a Windfall? Steps to Financial Security

- Tax Law Impacts: One Big Beautiful Bill Act

- Saltmarsh Financial Advisors Recognized as Top Wealth Advisory Firm

- Estate Planning Essentials

- Magnifying Single-Stock Volatility

- Markets Look Forward. So Should Investors.

- Father's Day: Money Lessons Learned From Dad

- Why You May Need a Revocable Trust

- Cost of Index Reconstitution: Index & Diversification Portfolios

- Three Tips for Riding Out the Ups and Downs: Investment Trends

- Bearish Sentiment: Investment Trends

- Tariffs and Stagflation

- How Extreme was Recent Large Growth Outperformance?

- View All Articles