Could You Be Owed a Refund for IRS Penalties or Interest During Covid?A Recent Tax Court Case May Open the Door to Relief for Some Taxpayers

5/22/2026 - By Michael Cole, JD, MSPA

{kind=link}

A recent federal court case, Kwong v. United States, is creating significant buzz in the tax world because it gives some taxpayers the ability to request refunds that were previously thought as unavailable. This is all because penalties and interest assessed during the COVID-19 pandemic may not apply to many taxpayers because of recent legislative and court determinations.

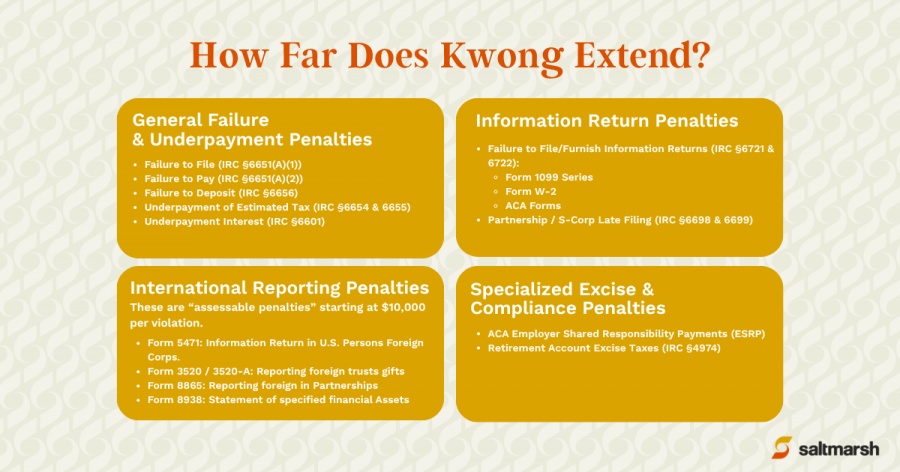

While the legal details are complex, the practical takeaway is simple if you have penalties from the following:

You may be eligible for a refund, but time is short! Taxpayers may have until July 10, 2026 to file protective refund claims related to penalties and interest charged during the pandemic years.

What Did the Court Decide?

Normally, taxpayers only have a limited amount of time to:

- Request refunds from the IRS

- Challenge penalties or interest assessments

- File tax refund lawsuits

In Kwong, however, the court determined that the COVID disaster declaration effectively paused portions of those deadlines from January 20, 2020 through July 10, 2023, giving taxpayers the opportunity to get previously applied penalties and interest refunded.

Why is everyone talking about July 10, 2026?

Under the court’s reasoning, many refund limitation periods may now extend three years beyond July 10, 2023 - creating a potential filing deadline of July 10, 2026.

However, this is not a universal deadline for every taxpayer or every tax issue. Eligibility depends on several factors, including:

- When the tax, penalty, or interest was paid

- Whether a refund claim was previously filed

- Whether the taxpayer was located in a covered disaster area during COVID

- Whether the issue involves a refund claim or an unpaid assessment

Important Limitations to Understand

Although the Kwong decision is taxpayer-friendly, it is not a blanket waiver of all IRS deadlines.

A few important cautions:

- The case involved very specific procedural tax rules

- Different IRS deadlines operate differently

- Some taxpayers may still be outside the allowable refund period

- The IRS has not broadly conceded this position

- Additional appeals or future court decisions could affect how broadly the ruling applies

In other words, taxpayers should not assume they automatically qualify for relief - but they also should not assume they are out of options.

What Taxpayers Should Do Now

If you paid IRS penalties or interest during the COVID years, it may be worth reviewing whether you could still qualify for a refund claim. Refund opportunities may be available to a wide range of taxpayers, including individuals, C corporations, S corporations, and partnerships.

Our team is uniquely qualified to determine if it is in your best interest to file a protective claim to preserve your refund rights. These rules are highly technical and fact-specific, so taxpayers should consult with a qualified tax advisor before taking action.

If you believe you may qualify for relief - or simply want help determining whether these rules apply to you - contact us to discuss your options before potential deadlines expire.

Final Takeaway

The Kwong case may become one of the more significant recent taxpayer-favorable procedural tax decisions because it potentially reopens opportunities that many believed had already expired. We are not issuing tax advice or composing a tax opinion on the matter, but we are actively working to ensure our clients make informed decisions about refunds for penalties and interest incurred during the COVID period.

Our Team's Experience

Michael Cole, JD, MSPA

Partner

Michael has an extensive background leveraging complex tax matters and tax law to help businesses and individuals navigate sophisticated planning, structuring, and advisory challenges. With experience spanning mergers and acquisitions, private equity transactions, entity structuring, and multi-faceted tax strategies, Michael is known for translating highly technical tax issues into practical, business-focused guidance that helps clients make informed decisions in an evolving regulatory environment. Learn more

David Uslan, CPA

Partner

David has more than 30 years of experience advising high-net-worth individuals, business owners, and closely held companies on complex tax and financial matters. Having previously worked with large national accounting firms, David brings a broad perspective and deep technical knowledge to areas including tax planning, compliance, business advisory, and strategic consulting across industries such as real estate, professional services, legal, and technology. Learn more

Stacey Craig, CPA

Partner

Stacey has significant experience helping individuals and businesses navigate tax compliance, planning, and advisory matters. She works closely with clients to provide practical guidance in an evolving tax environment, with a focus on proactive solutions, responsiveness, and long-term client relationships. Learn more

Jarot Scarbrough, CVA, JD, LLM

Senior Manager

Jarot has broad experience advising businesses, high-net-worth individuals, and closely held companies on complex tax law and procedural tax matters. His work includes researching and analyzing emerging tax developments, helping clients evaluate potential opportunities for relief, and navigating nuanced IRS procedures and controversy-related matters with a practical, solutions-oriented perspective. Learn more

Related Posts

- Family Office Tax Planning

- Funding Liquidity Without Triggering Capital Gains

- Could You Be Owed a Refund for IRS Penalties or Interest During Covid?

- IRS Notice CP53E: What Is It & What to Do If You Receive One

- Introducing Our New Podcast: Integrated Wealth Perspectives

- Outsourced Accounting for Nonprofits

- Manufacturing Cash Flow Forecasting Services for Volatile Markets

- Church Accounting Services for Donor Tracking & Financial Transparency

- Real Estate Accounting Services for Cash Flow Visibility and Portfolio Performance

- Maximizing Your Home Office Deduction

- What CEOs and CFOs Need to Know About Outsourced Accounting Costs

- How Outsourced Accounting Helps Growing Businesses Scale with Confidence

- Are You 5500 Compliant? Key Considerations for Health & Welfare Plans

- Avoid Costly Bookkeeping Mistakes in Your Construction Projects

- What the Best Accounting Outsourcing Companies Provide that Bookkeepers Don't

- How an Outsourced Accounting Department Transforms Month-End Close

- Meals & Entertainment Expenses

- How Accounts Payable Outsourcing Improves Accuracy, Speed, and Internal Controls

- The Hidden Benefits of Accounts Receivable Outsourcing for Businesses

- IRS Releases FAQ on Paper Check Phase-Out

- Construction Accounting Methods Explained: Cash, Accrual, and Percentage-of-Completion

- Saltmarsh Leader Suzanne Bach Joins ABC Florida Gulf Coast Board

- The Final Chapter of the Estate Plan

- What to Know Before Year-End

- The End of Paper Refund Checks: Are You Ready for the IRS Digital Shift?

- View All Articles